You're standing in your living room in Colorado Springs, the sun is finally hitting the glass just right, and instead of the view you want, you see streaks, pollen, hard-water spots, and dust collecting in every corner. The windows need attention. Maybe the gutters do too. Maybe you've put it off because some of that glass is high, awkward, or not safe to reach.

At that point, most homeowners start by comparing prices. That makes sense. But there's a second question that matters just as much as the quote. If something goes wrong on your property, who's responsible?

That's where cleaning liability insurance enters the picture. For homeowners, property managers, and business owners searching for window cleaning near me, professional window cleaning, or window cleaning in Colorado Springs, CO, insurance isn't a side detail. It's one of the clearest signs you're hiring a real service company, not just someone with a ladder and a squeegee.

Why Insurance Matters When Hiring a Cleaning Service

A lot of people hire a cleaner or window washing company because they want one simple result. Clean glass without the hassle. That's fair. But the work itself happens around ladders, screens, walkways, landscaping, trim, fixtures, and sometimes delicate materials that can be damaged if the wrong method is used.

A normal service visit can involve more risk than homeowners realize. A hose crosses a walkway. A ladder foot shifts on uneven ground. A tool bumps painted trim. Water runs where it shouldn't. Most jobs go smoothly, but when a mistake happens, the cost and stress can land on the property owner if the company isn't properly insured.

Peace of mind matters as much as clean windows

Insurance changes the entire conversation. Instead of hoping everything goes right, you're hiring a company that has planned for the possibility that something could go wrong. That protects the business, but it also protects your home, your schedule, and your peace of mind.

For exterior services, this mindset matters even more. Residential window cleaning, exterior window cleaning, gutter cleaning, and pressure washing all involve physical work on and around your property. If a company treats insurance like an afterthought, it usually tells you something about how they handle safety, training, and accountability too.

Practical rule: If a company is comfortable working several stories up on your home, they should be just as comfortable showing proof of insurance.

That same principle shows up in related exterior services as well. Homeowners looking into roofline and drainage work often ask similar questions, which is why this guide on why licensed gutter cleaners provide peace of mind for homeowners resonates with so many people in Colorado Springs.

What homeowners are really buying

When you hire a professional for residential window cleaning or commercial window cleaning, you're not just buying cleaner glass. You're buying:

- Protection for your property when work is taking place near finished surfaces and landscaping

- A clear process if an accident, claim, or question comes up

- Professional accountability instead of vague promises

- Less personal risk for you as the owner or manager

That's why insurance is essential. It's part of what separates a legitimate service provider from a gamble.

What Is Cleaning Liability Insurance Really

Most homeowners hear the phrase cleaning liability insurance and assume it's a broad catch-all policy. In practice, what people usually mean is General Liability Insurance. Think of it as the business version of the liability portion of your home or auto policy. It's there to respond when the company's work causes harm to someone else or damages someone else's property.

For cleaning companies, that's the foundation. According to Market Intelo's commercial cleaning business insurance report, General Liability Insurance is the foundational coverage in the cleaning industry, and the average payout for a liability claim has reached $1,562 since 2020, with common claims involving slips, falls, and property damage.

What it usually responds to

If you're hiring a company for interior window cleaning, exterior window washing, screen cleaning, or track cleaning, general liability is usually intended to address third-party claims in a few broad categories:

| Type of issue | Plain-English example |

|---|---|

| Bodily injury | A visitor slips near a wet walkway during service |

| Property damage | Equipment or cleaning activity damages part of the home or building |

| Personal injury | A claim involving non-physical harm, such as reputational allegations |

The key point is simple. This coverage is designed for damage or injury involving other people or their property. That's why legitimate service companies carry it even when most jobs are routine and uneventful.

Why this matters in day-to-day window cleaning

Window cleaning sounds low drama until you think through the details. A tech may be moving ladders around decorative stone, stepping through planted beds, removing screens, working above patios, or cleaning near entry doors with regular foot traffic. Even careful teams need a backstop.

That's also why owners researching the business side of service companies often spend time learning about financial protection for cleaning entrepreneurs. It gives useful context for why serious operators don't treat insurance as optional overhead.

Proper insurance doesn't mean a company expects problems. It means they take responsibility seriously enough to prepare for them.

Why it should matter to homeowners and property managers

For local clients searching window cleaning in Colorado Springs, CO, insurance is one of the fastest filters you can use. If a company is vague about coverage, slow to provide proof, or dismissive when asked, that's worth noticing.

Professional window cleaning should leave your windows brighter, your screens cleaner, and your property better maintained. It shouldn't create uncertainty about what happens if something breaks, someone gets hurt, or a claim needs to be filed.

Understanding Policy Limits and Key Terms

Once you know a company carries cleaning liability insurance, the next question is how much coverage they possess. Many homeowners then get handed a Certificate of Insurance, glance at it, and feel none the wiser.

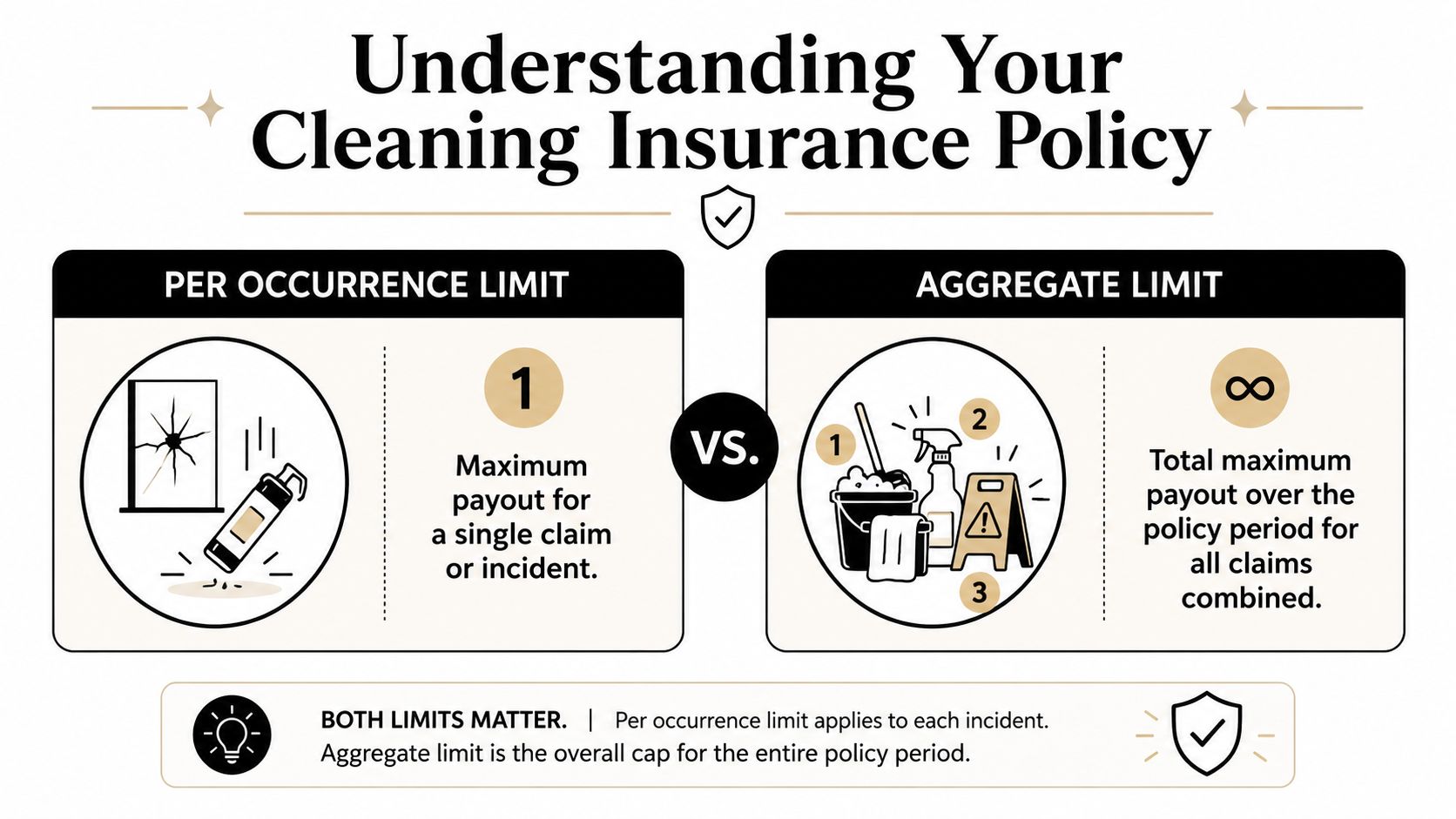

The two terms that matter most are per occurrence and aggregate. If you understand those, you can read the basics of a policy without getting lost in insurance language.

Per occurrence and aggregate in plain English

A useful way to think about it is this. A policy has a cap for one event and a cap for the whole policy period.

- Per occurrence means the maximum the policy will pay for a single claim or incident.

- Aggregate means the maximum the policy will pay in total during the policy term for all covered claims combined.

If a company has strong-looking insurance on paper but a low aggregate, multiple claims in a year could reduce what's left. That may not matter for a small one-person operation doing limited work, but it matters more for companies serving larger properties, more customers, or commercial accounts.

A benchmark property managers often expect

For commercial accounts, there's a practical standard many clients look for. According to the National Window Cleaning Authority's window cleaning insurance requirements page, commercial window cleaning contracts typically require at least $1,000,000 per occurrence and a $2,000,000 aggregate limit.

That doesn't mean every residential job requires the exact same contract language. It does give homeowners and property managers a useful benchmark for what professional-level coverage often looks like in the field.

What to look for on a certificate

When a company sends over proof of insurance, most clients don't need to decode every line. Start with the practical items:

- Business name match. The name on the certificate should match the company you're hiring.

- Effective dates. Make sure the policy is active on the date of service.

- Coverage type. Look for General Liability, at minimum, for this kind of work.

- Limits listed clearly. Check the per occurrence and aggregate amounts.

- Operations fit the work. If the company is doing exterior window cleaning, gutter cleaning, or related services, the policy should match real operations.

A clean-looking certificate isn't enough if the business name, dates, or coverage details don't line up with the work being performed.

Why this matters for local hiring decisions

In Colorado Springs, homeowners often need more than basic window washing. They may want hard water stain removal, screen cleaning, track cleaning, or service on taller homes with difficult access. Property managers may need recurring commercial window cleaning with proof of insurance on file.

Knowing how to read limits helps you compare providers based on more than appearance and price. It helps you tell the difference between someone who's ready for professional work and someone who just says they're insured.

The Hidden Gaps Most Cleaners Wont Mention

A company can say it's fully insured and still leave a major hole in protection. This is one of the most misunderstood parts of cleaning liability insurance, and it matters a lot for window cleaning.

The gap is called the care, custody, and control exclusion. In plain English, it can mean that the item being actively worked on isn't covered under a standard general liability claim.

Why this catches people off guard

Most homeowners hear “insured” and assume that if a cleaner damages a window while cleaning it, the insurance automatically pays. That assumption can be wrong.

A video explanation of the care, custody, and control exclusion points out a critical detail often missed in general liability policies. Damage to the specific item being worked on, such as a window being washed, can be denied because of this exclusion.

That means if a technician scratches glass, damages a screen frame during removal, or harms the very surface under active service, a standard policy may not respond the way the homeowner expects.

A real-world window cleaning example

This matters even more for professional window cleaning on larger homes and commercial properties. A fourth-story pane isn't the same as wiping fingerprints off a ground-floor slider. The access is harder, the glass replacement can be more complicated, and the stakes rise quickly when the exact item being serviced is expensive or specialized.

For homeowners and property managers, the takeaway is simple. “Insured” is not a complete answer. It's the start of the conversation, not the end.

Questions worth asking

Here are better questions than “Are you insured?”

- Does your policy address damage to the item being cleaned?

- Have you reviewed care, custody, and control exclusions with your agent?

- Do your endorsements match the services you offer?

- If glass or screens are damaged during service, what is the claims process?

Worth asking directly: “If the window itself is damaged while you're cleaning it, is that covered under your current policy setup?”

A professional company won't be annoyed by that question. They'll understand exactly why you're asking.

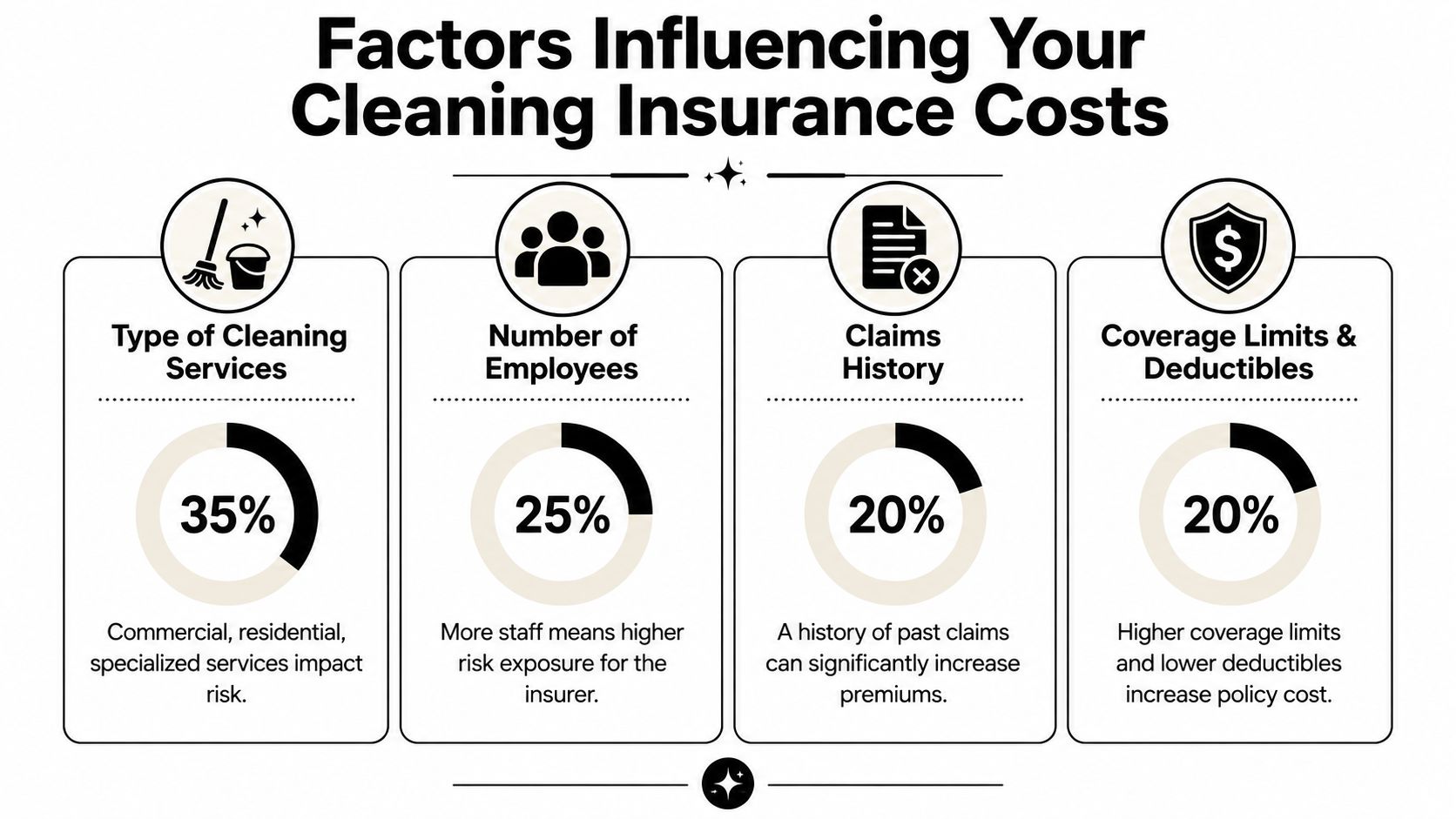

What Drives the Cost of Cleaning Insurance

Insurance pricing isn't random. Carriers price policies based on risk, and different cleaning services create very different kinds of exposure. That's why one company can pay much less than another even though both technically work in the cleaning industry.

For homeowners comparing bids for residential window cleaning or exterior window cleaning, this matters because a company's overhead often reflects how serious they are about operating safely and legitimately.

Risk profile changes the premium

The type of work matters a lot. A low-risk housekeeping operation isn't priced the same way as a company using ladders, water-fed poles, pressure washers, or roofline access equipment.

According to MoneyGeek's guide to general liability insurance for cleaning businesses, a standard house cleaning company may pay around $44 per month for liability insurance, while higher-risk services like pressure washing average closer to $75 per month because of the greater potential for property damage claims.

That comparison helps explain why specialized exterior cleaning companies often carry different insurance costs than a basic interior cleaning service.

The biggest cost drivers

Even without getting deep into underwriting, a few factors consistently move the price:

- Type of services offered. Pressure washing, gutter work, and cleaning at heights for exteriors usually create more risk than simpler interior tasks.

- Number of employees. More people on jobsites means more chances for accidents or claims.

- Claims history. Prior claims can affect how a carrier prices future coverage.

- Coverage limits and deductibles. Higher limits and lower deductibles generally cost more.

Why cheaper isn't always better

When a quote for window cleaning near me looks unusually low, it's fair to ask why. Sometimes the answer is efficiency and a lean business model. Sometimes the answer is less desirable. Limited coverage, mismatched operations, or bare-minimum policy choices can all reduce cost on paper.

A homeowner usually won't see those trade-offs in the estimate itself. They show up later, when there's a problem and the company either can't document coverage or discovers the policy doesn't fit the service performed.

What this means for service value

For services like streak-free window cleaning, screen cleaning, and maintenance visits, clients want a fair price. They also want confidence that the company has accounted for the risks of working around the property.

That's the trade-off. A lower quote may save money upfront. A better-insured professional often offers something less visible but more valuable. Fewer surprises if the job doesn't go perfectly.

Insurance for Colorado's Unique Cleaning Needs

Colorado Springs properties create a different set of challenges than a generic insurance article usually accounts for. Homes here often sit on slopes, face stronger sun exposure, collect wind-blown dust, and deal with seasonal debris that affects both windows and gutters. Add taller architecture, decks, retaining walls, and wildfire-conscious maintenance, and the insurance discussion changes.

That's especially true for companies offering more than basic interior window cleaning.

Height and terrain change the risk

A technician cleaning upper-story glass on a hillside property deals with a different environment than someone cleaning a flat suburban storefront. Access matters. Ladder placement matters. Surface conditions matter. The chance of damaging trim, screens, landscaping, or adjacent features rises when the property itself is more complex.

For homeowners seeking window cleaning in Colorado Springs, CO, this is one reason local experience matters. The company isn't just cleaning glass. They're working around the realities of Front Range homes and commercial buildings.

Gutter cleaning and fire mitigation need more than a basic policy

Colorado also brings service categories that many standard cleaning guides barely mention. Gutter cleaning and fire-mitigation clearing can involve working at height, removing vegetation, and creating concerns that don't always show up while the crew is still onsite.

According to Insurance Canopy's article on common gaps in house cleaner insurance, specialty services common in Colorado, such as fire-mitigation clearing and gutter cleaning, often require a completed operations endorsement and higher policy limits, because standard liability policies may not cover claims arising after the job is finished.

That distinction matters. A claim tied to completed work can look very different from a claim tied to something that happened during the service visit itself.

In Colorado, the question isn't only whether a company has insurance. It's whether the policy fits the actual work being done on the property.

Why local property owners should care

Homeowners in neighborhoods with defensible-space concerns and property managers responsible for ongoing exterior maintenance should be especially careful with this. A company may be excellent at window washing but underprepared for fire-mitigation clearing or drainage-related work if its policy was built around a narrower service menu.

For broader legal context, some property owners also find it helpful to review Nares Law Group on Colorado insurance, especially when they want a better understanding of liability issues under Colorado conditions.

A smarter hiring standard for local projects

If the work involves anything beyond straightforward glass cleaning, ask whether the company's insurance reflects:

- Gutter cleaning and roofline access

- Fire-mitigation clearing

- Post-service claims tied to completed operations

- The actual service list shown on the estimate

That's how you match the policy to the property instead of relying on a generic “we're insured” answer.

How to Confidently Verify Your Cleaner's Insurance

Asking for proof of insurance isn't awkward. It's normal. Good companies expect it, especially when they're providing commercial window cleaning, working on taller homes, or handling repeat maintenance for property managers.

The document you'll usually receive is a Certificate of Insurance, often called a COI. It's a summary document that shows key policy details without requiring you to read the full insurance contract.

What to check first

When the COI arrives, slow down and read the practical items.

- Company identity. Confirm the insured business name matches the company you contacted.

- Policy dates. Active coverage dates should include your service date.

- Coverage listed. Make sure General Liability appears clearly.

- Limits shown. Review the listed limits and make sure they fit the scope of work.

- Services align. If the company is performing specialty work, ask whether the policy setup reflects that scope.

These simple checks catch a surprising number of issues. A certificate can look official while still being outdated, tied to another entity, or too narrow for the job.

How to ask without making it awkward

You don't need legal language. A short message works:

“Before we schedule, would you send over your current Certificate of Insurance for our records?”

Professional companies hear that all the time. Property managers, HOAs, and commercial clients ask for it routinely. Homeowners should feel just as comfortable doing the same.

If you're already building a shortlist of questions before hiring, this guide on questions every homeowner should ask before hiring a window cleaning service fits naturally into that process.

A useful way to sanity-check a business

Insurance proof is one piece of legitimacy. Communication, local presence, and business documentation matter too. If you want a broader consumer checklist, this article from Recepta.ai on how to check if a company is legitimate is a practical companion resource.

For clients who want a quick visual overview of what insurance documents usually look like in practice, this short video helps:

Signs you're dealing with a professional

The easiest companies to work with on insurance questions usually share a few habits:

| Good sign | What it tells you |

|---|---|

| Fast response to COI requests | They handle this regularly |

| Clear explanation of coverage | They understand their policy |

| No defensiveness | They treat verification as standard |

| Consistent business details | Their paperwork matches their operations |

If a company dodges the request, sends partial information, or acts irritated that you asked, pay attention. Insurance transparency is often a good proxy for overall professionalism.

For homeowners booking seasonal window cleaning, screen cleaning, or recurring exterior maintenance in Colorado Springs, verification is the final confidence check before saying yes.

If you're looking for insured, professional exterior care in Colorado Springs and nearby communities, Cultivate House Detailing is ready to help with residential and commercial window cleaning, exterior window washing, screen repair, gutter cleaning, pressure washing, and fire-mitigation clearing. Reach out for a quote, ask questions, and get the peace of mind that comes from hiring a local company that takes protection, communication, and clean results seriously.